Form No. 60 for Form of Declaration In Respect of Permanent Account Number. Form No. 60 is relevant to persons who do not have permanent account number and who enter into any of the transactions specified in rule 114B. Such persons should fill up this form, verify and signed the declaration, and which transaction will not be put through. In case if you are not having PAN Card then now you can Apply Online PAN Card Application or You can do Download Form 49A for in PDF Format for PAN card

Every person shall quote his permanent account number in all documents pertaining to the transactions specified below, namely:—

(a) sale or purchase of any immovable property valued at five lakh rupees or more;

(b) sale or purchase of a motor vehicle or vehicle, as defined in clause (28) of section 2 of the Motor Vehicles Act, 1988 (59 of 1988), which requires registration by a registering authority under Chapter IV of that Act :

Provided that for the purposes of this clause, the sale or purchase of a motor vehicle or vehicle does not include two wheeled vehicles, inclusive of any detachable side-car having an extra wheel, attached to the motor vehicle;

(c) a time deposit, exceeding fifty thousand rupees, with a banking company to which the Banking Regulation Act, 1949 (10 of 1949), applies (including any bank or banking institution referred to in section 51 of that Act);

(d) a deposit, exceeding fifty thousand rupees, in any account with Post Office Savings Bank;

(e) a contract of a value exceeding one lakh rupees for sale or purchase of securities as defined in clause (h) of section 2 of the Securities Contracts (Regulation) Act, 1956 (42 of 1956);

(f) opening an account not being a time-deposit referred to in clause (c) with a banking company to which the Banking Regulation Act, 1949 (10 of 1949), applies (including any bank or banking institution referred to in section 51 of that Act);

(g) making an application for installation of a telephone connection (including a cellular telephone connection);

(h) payment to hotels and restaurants against their bills for an amount exceeding twenty-five thousand rupees at any one time ;

(i) payment in cash for purchase of bank drafts or pay orders or banker’s cheques from a banking company to which the Banking Regulation Act, 1949 (10 of 1949), applies (including any bank or banking institution referred to in section 51 of that Act) for an amount aggregating fifty thousand rupees or more during any one day;

(j) deposit in cash aggregating fifty thousand rupees or more, with a banking company to which the Banking Regulation Act, 1949 (10 of 1949), applies (including any bank or banking institution referred to in section 51 of that Act) during any one day;

(k) payment in cash in connection with travel to any foreign country of an amount exceeding twenty-five thousand rupees at any one time.

Explanation.—For the purposes of this clause,—

(a) “payment in cash in connection with travel” includes payment in cash towards fare, or to a travel agent or a tour operator, or to an authorized person as defined in clause (c) of section 2 of the Foreign Exchange Management Act, 1999 (42 of 1999), or for the purchase of foreign currency;

(b) the expression “travel to any foreign country” does not include travel to the neighbouring countries or to such places of pilgrimage as may be specified by the Board under Explanation 3 of sub-section (1) of section 139;

(l) making an application to any banking company to which the Banking Regulation Act, 1949 (10 of 1949), applies (including any bank or banking institution referred to in section 51 of that Act) or to any other company or institution, for issue of a credit or debit card;

(m) payment of an amount of fifty thousand rupees or more to a Mutual Fund for purchase of its units;

(n) payment of an amount of fifty thousand rupees or more to a company for acquiring shares issued by it;

(o) payment of an amount of fifty thousand rupees or more to a company or an institution for acquiring debentures or bonds issued by it;

(p) payment of an amount of fifty thousand rupees or more to the Reserve Bank of India, constituted under section 3 of the Reserve Bank of India Act, 1934 (2 of 1934) for acquiring bonds issued by it;

(q) payment of an amount aggregating fifty thousand rupees or more in a year as life insurance premium to an insurer as defined in clause (9) of section 2 of the Insurance Act, 1938 (4 of 1938);

(r) payment to a dealer,—

(i) of an amount of five lakh rupees or more at any one time; or

(ii) against, a bill for an amount of five lakh rupees or more,

for purchase of bullion or jewellery :

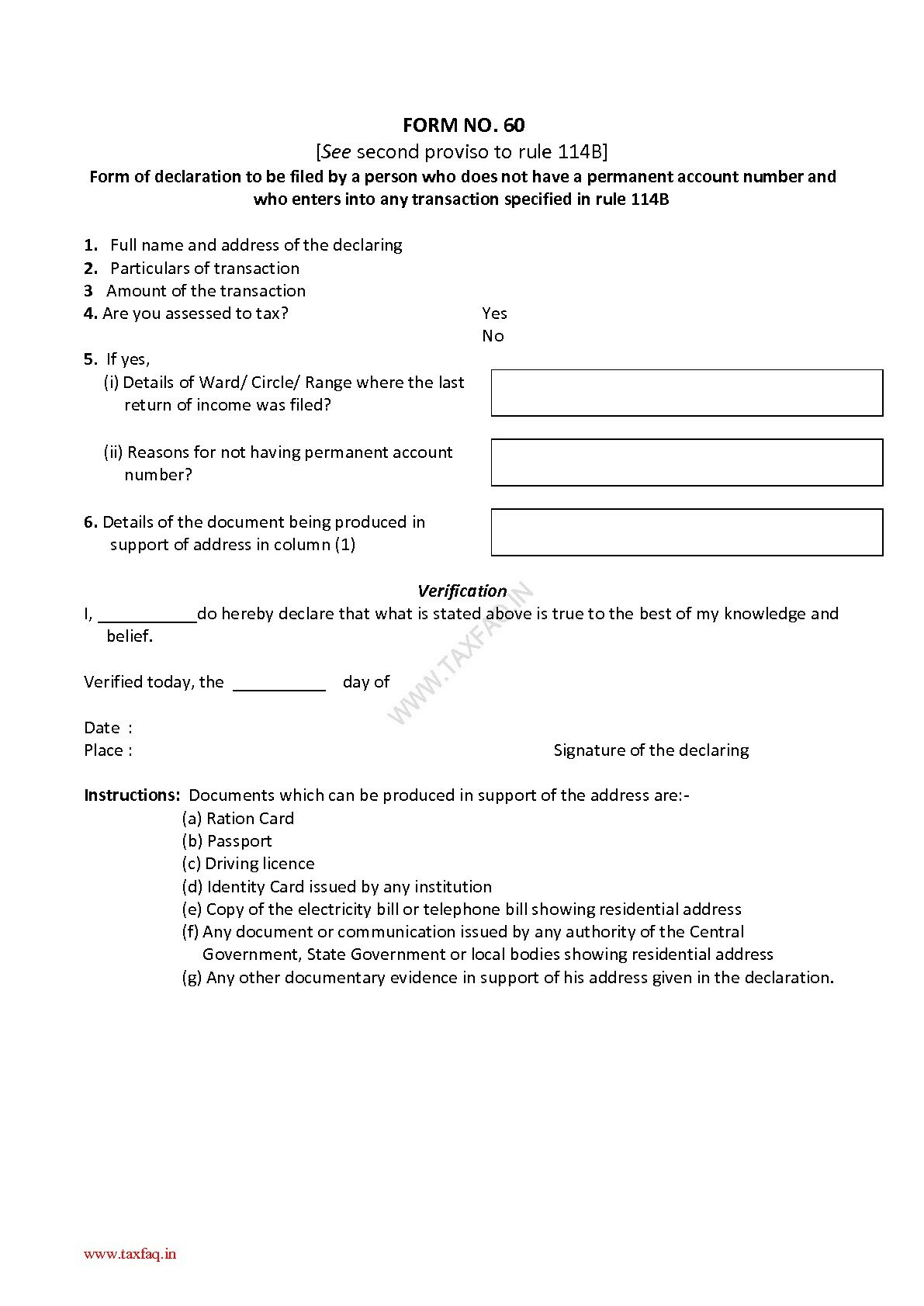

FORM NO. 60

[See second proviso to rule 114B]

Form of declaration to be filed by a person who does not have a permanent account number and who enters into any transaction specified in rule 114B

1. Full name and address of the declaring

2. Particulars of transaction

3 Amount of the transaction

|

4. Are you assessed to tax? |

Yes No |

5. If yes,

|

(i) Details of Ward/ Circle/ Range where the last return of income was filed? |

|

(ii) Reasons for not having permanent account number? |

|

6. Details of the document being produced in support of address in column (1) |

Verification

I,

do hereby declare that what is stated above is true to the best of my knowledge and belief.

| Verified today, the day of |

|

Date : |

|

| Place : |

Signature of the declaring |

Instructions: Documents which can be produced in support of the address are:-

(a) Ration Card

(b) Passport

(c) Driving licence

(d) Identity Card issued by any institution

(e) Copy of the electricity bill or telephone bill showing residential address

(f) Any document or communication issued by any authority of the Central Government, State Government or local bodies showing residential address

(g) Any other documentary evidence in support of his address given in the declaration.

good